Recently I had a fascinating lunch with some young and bright minds, with plenty of foresight. One of the things we discussed was neurodivergence and its link to the finance industry, especially in value investing: a niche and highly technical sector. As a parent who has spent the past good 10 years learning about, and advocating for, the neurodivergent community, I find it especially interesting. Why? Let me explain.

Measuring Minds

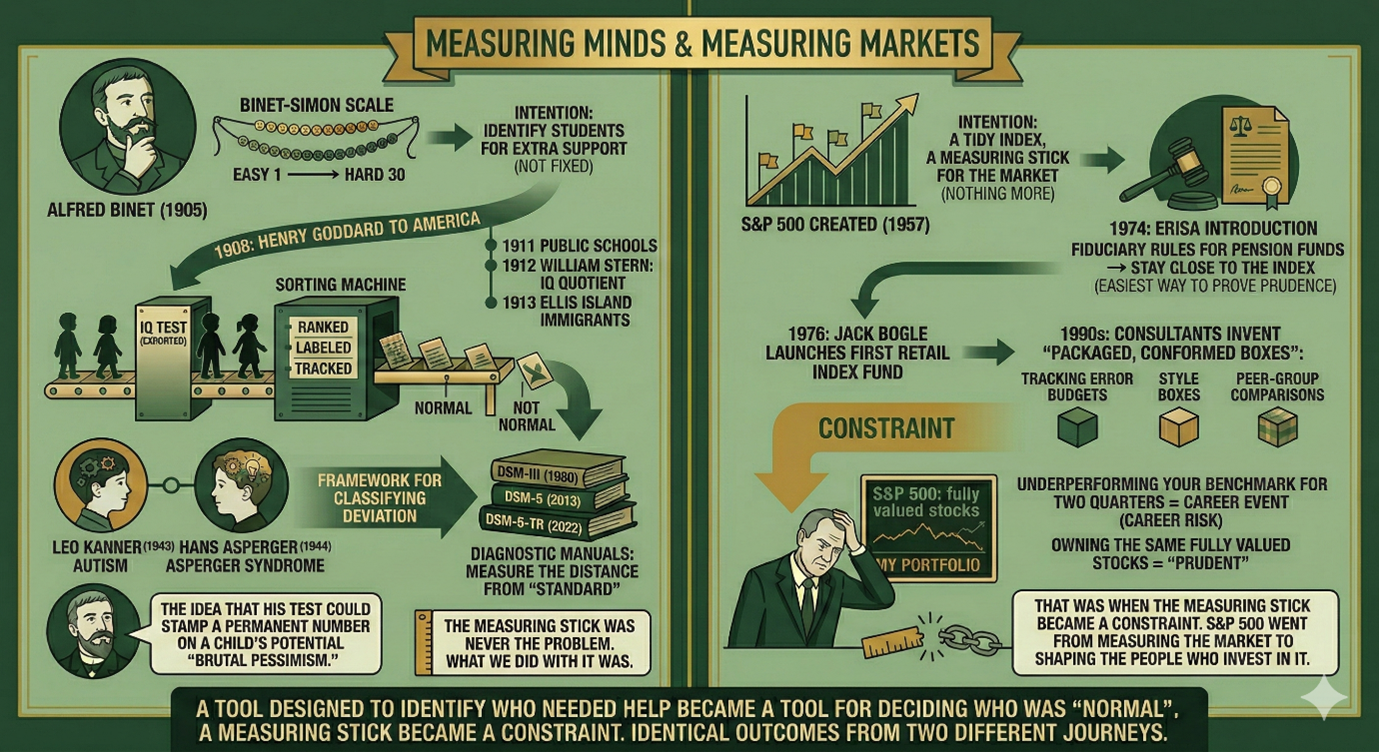

In 1905, a French psychologist named Alfred Binet was asked to solve a practical problem: which schoolchildren in Paris needed extra support? So he built a test containing 30 simple tasks, arranged from easy to hard. It was never meant to define a child — it was meant to help one.

In 1908, Henry Goddard travelled to Europe, discovered Binet’s test, brought it back to the Vineland Training School in New Jersey, translated it into English, and published his version in December 1908. By 1911 it was in public schools, by 1912 William Stern had turned it into the IQ quotient, and by 1913 Goddard was administering it to immigrants at Ellis Island. In other words, Binet’s measuring tool had been exported to America, repackaged as the IQ test, and turned into something he never intended: a sorting machine. Children were ranked, labelled, and tracked.

A tool designed to identify who needed help became a tool for deciding who was “normal” and who wasn’t.

By the time Leo Kanner described autism in 1943, and Hans Asperger independently described similar children in Vienna a year later (hence the term “Asperger Syndrome”), the framework was already in place. Not a framework for understanding how different minds work, but for classifying how far they deviate from an expected norm. The diagnostic manuals that followed — from the DSM-III in 1980 to the DSM-5 in 2013, and its text revision in 2022 — refined the categories. But the underlying logic remained: measure the distance from “standard.” Define the deviation.

I would imagine Binet himself would have hated this. He believed intelligence was changeable, not fixed. He called the idea that his test could stamp a permanent number on a child’s potential “brutal pessimism.”

The measuring stick was never the problem. What we did with it was.

Measuring Markets

The finance industry did exactly the same thing.

In 1957, the S&P 500 was created. It started out as a tidy index of 500 American companies, designed as a measuring stick for the market. Nothing more. In 1974, ERISA introduced fiduciary rules for pension funds, and the easiest way to prove you weren’t being reckless was to stay close to the index. In 1976, Jack Bogle launched the first retail index fund. By the 1990s, consultants had invented tracking error budgets, style boxes, and peer-group comparisons — and packaged them in a neat, conformed box.

As a result, a generation of fund managers learned that underperforming your benchmark for two quarters was a career event, but owning the same fully valued stocks as everyone else was “prudent.” (Hence, we constantly talk about ONE big, realistic risk for allocators picking emerging managers: the career risk.)

That was when the measuring stick became a constraint. And just as Binet’s test went from helping children to sorting them, the S&P 500 went from measuring the market to shaping the people who invest in it.

The Neurodivergent Edge

Here’s where these two histories meet.

The qualities that make someone benchmark-agnostic — the ability to tune out consensus, to fixate on a single idea with unusual depth, to feel genuinely uncomfortable following a crowd, to hold a contrarian position long after the social pressure says “conform” — these overlap remarkably with traits associated with neurodivergence.

My personal favorite is pattern recognition that others miss: connecting dots amongst thousands of them. My second is the ability to hyperfocus on details that most analysts skim past (this rings especially true in the European SMID-cap space, where so much is overlooked and misunderstood). An almost physical discomfort with doing something just because everyone else is doing it. A willingness — and in most cases an inability to do otherwise — to think in systems rather than narratives.

I’m not saying every great investor is neurodivergent. But I am saying that the investment industry spent fifty years building a system that rewards conformity — and the people who’ve consistently beaten it tend to be the ones who were never wired for conformity in the first place.

That’s not a coincidence. In both fields — education and finance — the people who thrived most were the ones the measuring tools were least equipped to understand.

--Jenny Ngan, Head of Business Development